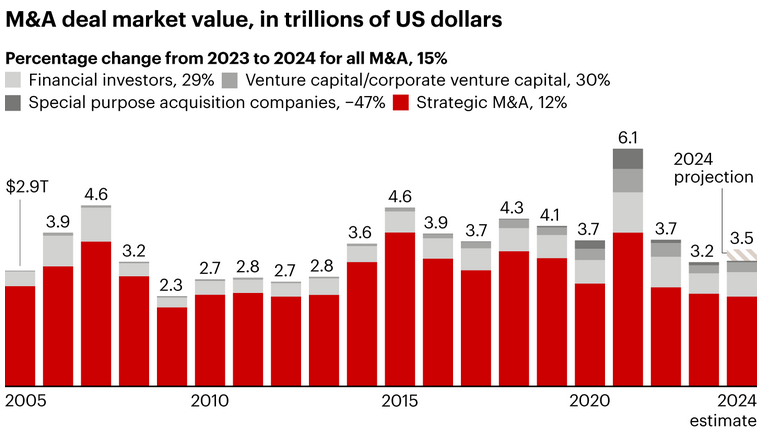

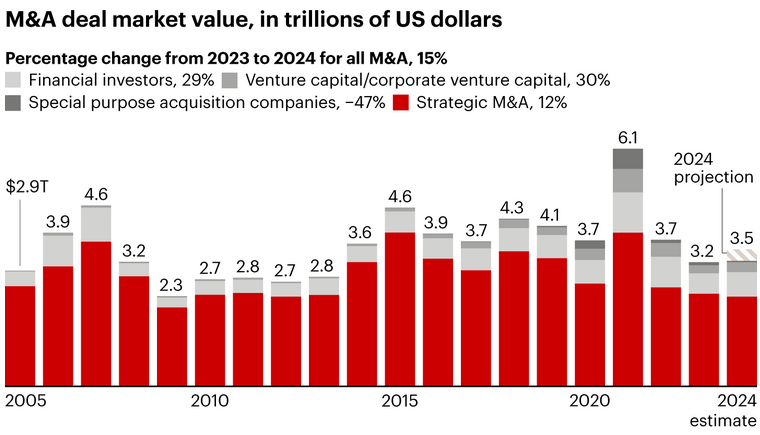

The global M&A market in 2024 demonstrated a modest recovery, with total deal value reaching approximately $3.5 trillion, reflecting a 15% increase year-over-year.

Source: Dealogic, as of December 2nd, 2024

While macroeconomic headwinds such as inflation, high interest rates, and regulatory scrutiny persisted, corporates and financial sponsors adapted their strategies, focusing on high-value sectors, cross-border deals, and portfolio simplifications. These shifts have set the stage for a promising outlook in 2025, contingent on stabilizing economic and regulatory environments.

Key Highlights in 2024

Large-Scale Deals and Regional Dynamics

- Large Transactions in the U.S.: Mega-deals ($10 billion+) drove growth, increasing by 26% globally, with the U.S. leading activity in technology, healthcare, and financial services. However, a lack of attractive domestic targets due to private equity sponsors’ reluctance to exit prompted corporates to explore international markets.

Source: Goldman Sachs, December 2024

- Cross-Border Surge: APAC accounted for 30% of global deal volumes, fueled by the China+1 strategy, which emphasized diversification to Vietnam, India, and Indonesia. These countries attracted inflows due to favorable valuations, regulatory incentives, and expanding consumer markets

- European Activity: EMEA experienced a 43% year-on-year increase in large-scale deals, driven by portfolio transformations and simplifications.

Source: Goldman Sachs, December 2024

Sectoral Shifts

- Energy: The energy sector pivoted towards scale consolidation, with companies focusing on cost efficiencies and market share growth. This shift addressed challenges from rising operational costs and environmental pressures.

- Technology: Technology remained a focal point, with companies pursuing growth-oriented scope deals. Investments concentrated on enhancing capabilities in artificial intelligence, digital transformation, and cloud infrastructure. Although activity slowed compared to the 2020–2021 boom, the sector’s relevance persisted.

- Consumer Products: In a challenging market defined by rising prices and uncertain demand, consumer products companies aimed to restore profitable, volume-led growth by reviving consumer confidence and adapting to shifting preferences.

- Healthcare: Healthcare continued to attract significant M&A, with deals emphasizing scalability and innovation to meet demographic shifts and rising healthcare demands.

Source: Dealogic, as of December 2nd, 2024

- Corporate Simplification

- Companies prioritized spin-offs and divestitures of non-core or geographically dispersed assets to reduce complexity, unlock value, and sharpen focus on high-growth industries.

- Activist investors played a pivotal role in driving these strategies.

- Private Equity Trends

- Sponsors deployed dry powder strategically, favoring carve-outs and take-private transactions, particularly in EMEA and APAC. However, exits remained cautious due to valuation mismatches and an uncertain macroeconomic environment.

- Regulatory Challenges

- Stringent regulatory scrutiny, particularly in the U.S. and Europe, extended deal timelines and influenced deal structures. Companies adapted by focusing on upfront regulatory risk assessments and pursuing transactions with lower complexity.

Key Trends in 2025

- Cross-Border Momentum

- Cross-border M&A is expected to intensify, with APAC and SEA remaining key destinations for corporations seeking diversification and growth. Vietnam, India, and Indonesia will benefit from continued interest driven by the China+1 strategy, valuation arbitrage, and favorable policy environments. Cross-border deals will focus on high-growth sectors such as technology, consumer goods, and industrial.

- Sectoral Focus on Growth Industries

- AI and Technology: Investments will shift from infrastructure to application-layer AI, focusing on generative AI tools that enhance workflows and drive efficiency. Cloud computing, semiconductors, and cybersecurity will also attract heightened activity.

- Healthcare: Innovation and scalability will remain priorities, as companies address demographic shifts and seek to adopt advanced technologies.

- Energy and Sustainability: Increased emphasis on renewable energy and ESG-related acquisitions will align with global sustainability goals.

- Simplification and Portfolio Optimization

- Simplifications will evolve into more targeted regional realignments and sectoral transformations. Newly independent entities from spin-offs are likely to engage in follow-on M&A to pursue growth opportunities. Activist investors will continue to drive simplifications for shareholder value creation.

- Generative AI adoption in M&A processes will accelerate, enabling early adopters to reduce manual effort, shorten timelines, and improve due diligence. This will enhance efficiency across the deal lifecycle and provide a competitive edge to tech-savvy deal makers.

- Regulatory Adjustments

- The regulatory environment is anticipated to stabilize, fostering CEO confidence and reducing deal delays. Companies will continue investing in pre-deal regulatory risk assessments to navigate approval processes effectively.

Conclusion

The M&A landscape in 2025 is poised for accelerated growth, driven by cross-border transactions, sectoral realignments, and technology-led transformations. Corporations will continue to focus on international expansions and capability-enhancing acquisitions, while private equity sponsors navigate a balance between deploying capital and pursuing exits. Emerging markets in Southeast Asia, coupled with stabilizing regulatory and economic conditions, present significant opportunities for value creation.

With a clear focus on growth, simplification, and technology, 2025 promises to be a transformative year for global deal making. The emphasis on AI adoption, sustainability, and regional diversification will define the next wave of M&A activity, ensuring a dynamic and resilient market.